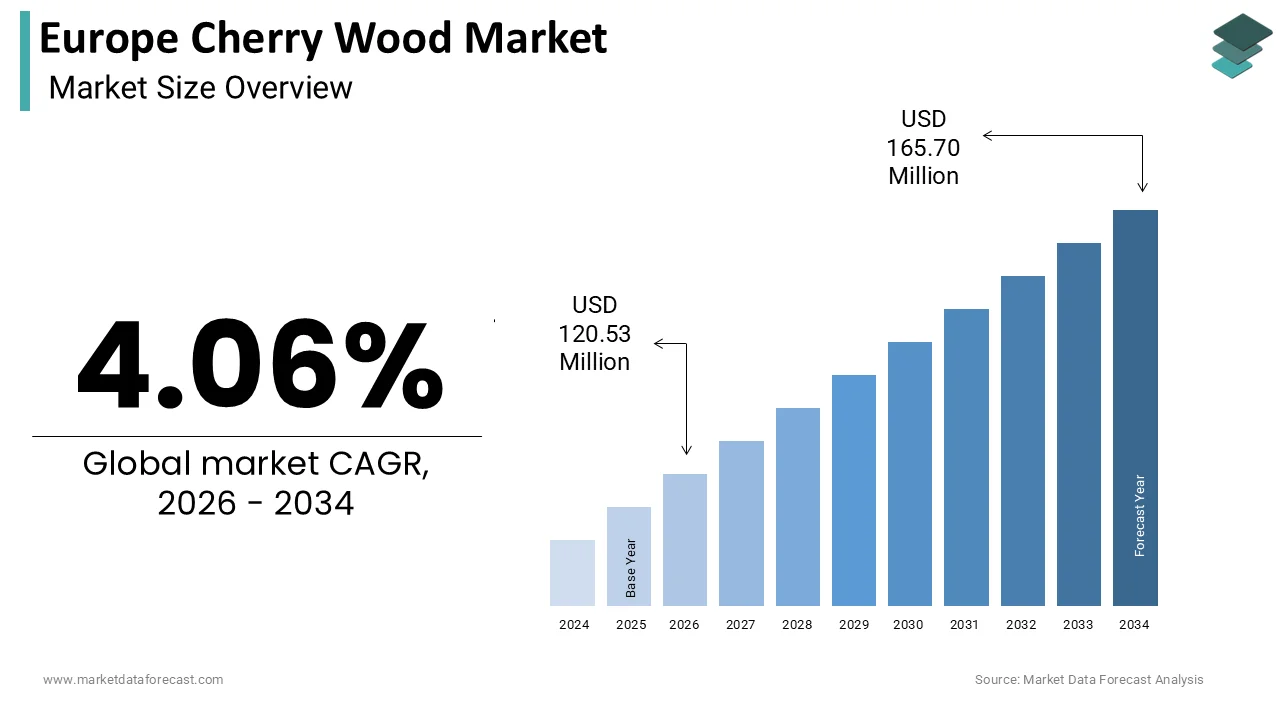

The Europe cherry wood market size was calculated to be USD 115.83 million in 2025 and is anticipated to be worth USD 165.70 million by 2034, from USD 120.53 million in 2026, growing at a CAGR of 4.06% during the forecast period.

The cherry wood is rich reddish-brown hue, fine grain, and exceptional workability. This premium hardwood serves as a cornerstone for high-end furniture manufacturing, luxury interior joinery, and specialized musical instrument production across the continent. The region boasts significant natural reserves, with European forests covering approximately 227 million hectares, where cherry trees constitute a valuable but limited component of mixed deciduous stands according to Forest Europe data. In 2024, the sustainable management of these resources remained a priority, with over 60% of European forest area certified under schemes like PEFC or FSC to ensure ecological balance as per the Confederation of European Paper Industries. Furthermore, the woodworking sector in countries like Italy and France consumes substantial volumes of this timber for restoration projects, adhering to strict heritage conservation guidelines that mandate the use of authentic materials.

MARKET DRIVERS

Resurgence of Bespoke Luxury Furniture and Interior Design

The revitalization of the bespoke luxury furniture sector by affluent consumers seeking unique, handcrafted pieces that exude warmth and sophistication is escalating the growth of Europe cherry wood market. High-net-worth individuals increasingly favor custom-made cabinetry, dining tables, and bedroom suites crafted from solid cherry wood due to its ability to develop a deep patina over time, enhancing its visual appeal. Designers specifically select cherry wood for its stability and ease of finishing, which allows for intricate carving and smooth polishing essential for high-end aesthetics. The trend toward “quiet luxury” emphasizes quality materials over ostentatious branding, further boosting the preference for natural hardwoods. Additionally, the renovation of historic properties in cities like Paris, Vienna, and Rome necessitates the use of traditional materials to maintain architectural integrity, creating a steady stream of demand for restoration-grade cherry timber. This shift away from synthetic alternatives toward authentic, durable materials ensures a robust and resilient demand base for cherry wood artisans and suppliers.

Expansion of the Premium Musical Instrument Manufacturing Sector

The sustained demand from the premium musical instrument industry, where cherry wood is prized for its acoustic properties and aesthetic versatility in crafting guitars, violins, and woodwind instruments, is accelerating the growth of Europe cherry wood market. Luthiers across Europe value cherry wood for its balanced tonal characteristics, offering a warm mid-range response similar to mahogany but with a distinct visual identity that appeals to modern musicians. In 2024, the European market for handcrafted musical instruments generated revenue exceeding 2.4 billion euros, with a notable segment dedicated to custom and semi-custom instruments utilizing native hardwoods, according to the International Music Products Association. The revival of traditional craftsmanship in countries such as Germany and Czechia has led to a resurgence in small-scale workshops that prioritize locally sourced materials to reduce carbon footprints and support regional forestry. The scarcity of traditional tropical hardwoods due to logging restrictions has also prompted instrument makers to explore European alternatives, positioning cherry wood as a viable and ethical substitute. This alignment of acoustic performance, ethical sourcing, and artistic tradition secures a specialized but lucrative demand channel for the cherry wood market.

MARKET RESTRAINTS

Prolonged Growth Cycles and Limited Natural Availability

The inherently long rotation period required for cherry trees to reach commercial maturity, which severely limits the annual supply volume, is limiting the growth of Europe cherry wood market. Unlike fast-growing softwoods or plantation species, Prunus avium typically requires 40 to 60 years to develop the diameter and heartwood quality necessary for high-value applications by creating a structural bottleneck in supply responsiveness. This scarcity is exacerbated by the fact that cherry trees rarely grow in pure stands, instead appearing as scattered individuals within mixed deciduous forests, which complicates logging operations and increases extraction costs. Foresters often prioritize more abundant species like oak or beech for economic efficiency by leaving cherry wood as a secondary harvest target. Consequently, any surge in demand cannot be met with immediate supply increases, leading to price volatility and potential shortages for manufacturers. This biological constraint fundamentally caps the market’s expansion potential, forcing industries to rely on existing stockpiles or seek alternative materials when supply tightens.

Stringent Environmental Regulations and Logging Restrictions

Strict environmental regulations and sustainable forestry mandates across the European Union act as a formidable restraint on the harvesting and trade of cherry wood, limiting the volume of timber entering the market. The EU Biodiversity Strategy for 2030 aims to strictly protect old-growth forests and increase the proportion of protected areas to 30% of the land surface, which often includes habitats where mature cherry trees thrive. In 2024, several member states implemented tighter controls on logging activities in sensitive ecological zones, resulting in a reduction in permissible harvest quotas for certain hardwood species, as reported by the European Environment Agency. Compliance with these regulations requires extensive documentation and certification, adding administrative burdens and costs for forestry operators and timber merchants. The requirement for Chain of Custody certification under FSC or PEFC schemes further restricts market access for non-compliant suppliers, effectively shrinking the pool of available legal timber. Additionally, restrictions on the use of heavy machinery in protected areas to prevent soil compaction and biodiversity loss increase the logistical complexity and expense of extracting scattered cherry trees. While essential for conservation, these measures create a supply-side constraint that hampers the market’s ability to scale operations efficiently.

MARKET OPPORTUNITIES

Development of High-Value Engineered Wood Products

The innovation and commercialization of high-value engineered wood products that maximize the utility of limited cherry timber resources are substantially creating new opportunities for the growth of Europe cherry wood market. By utilizing advanced lamination and veneer technologies, manufacturers can create stable, large-format panels and decorative surfaces that retain the aesthetic qualities of solid cherry while using significantly less raw material. This approach allows producers to stretch the supply of scarce cherry logs by slicing them into thin veneers that can cover vast surface areas for flooring, wall cladding, and furniture facades. The development of cross-laminated timber (CLT) incorporating cherry layers offers new structural and aesthetic possibilities for high-end architectural projects, opening up applications previously dominated by softwoods. Furthermore, the use of finger-jointing techniques enables the creation of long, defect-free boards from smaller offcuts, reducing waste and improving yield efficiency. This technological shift not only addresses supply constraints but also appeals to eco-conscious consumers seeking sustainable luxury, positioning engineered cherry wood as a growth engine for the future of the industry.

Revival of Traditional Craftsmanship and Heritage Restoration Projects

The increasing emphasis on cultural heritage preservation and the revival of traditional craftsmanship, particularly in the restoration of historical buildings and antique furniture, is expected to set up new opportunities for the growth of Europe cherry wood market. Governments and private entities are investing heavily in the conservation of historic sites, mandating the use of authentic materials that match the original construction to maintain historical accuracy. Cherry wood, with its historical prevalence in 18th and 19th-century European furniture and joinery, is often the specified material for these restorations due to its unique color and grain pattern. This creates a specialized, high-margin market segment where price sensitivity is low, and quality is paramount. Additionally, the growing appreciation for artisanal skills has spurred a renaissance in woodworking schools and guilds, fostering a new generation of craftsmen who prefer working with traditional hardwoods. The demand for reclaimed cherry wood from demolished historic structures also offers a sustainable source of high-quality timber, appealing to developers seeking LEED certification for adaptive reuse projects.

MARKET CHALLENGES

Vulnerability to Climate Change and Pest Infestations

The escalating impacts of climate change, which exacerbates the susceptibility of cherry trees to drought stress, fungal diseases, and pest infestations is one of the challenges for the growth of Europe cherry wood market. Rising temperatures and altered precipitation patterns have weakened the natural defenses of Prunus avium by making it increasingly vulnerable to attacks by the cherry fruit fly and various bark beetles that thrive in warmer conditions. Drought events have stunted growth rates, extending the time required for trees to reach harvestable size and reducing the overall quality of the timber produced. Furthermore, the spread of invasive pathogens such as bacterial canker has devastated young plantations, threatening future supply pipelines. The European Forest Institute warns that without adaptive management strategies, the geographic range suitable for healthy cherry cultivation could shrink by 15% by 2040. These biological threats introduce significant uncertainty into supply forecasting, making it difficult for investors and manufacturers to plan long-term projects. The cost of mitigating these risks through enhanced silviculture and pest control measures further erodes profit margins, challenging the economic viability of cherry wood production in an increasingly volatile climatic environment.

Intense Competition from Alternative Hardwoods and Synthetic Substitutes

The intense competition from both alternative domestic hardwoods and advanced synthetic materials that offer similar aesthetic qualities at lower price points and with greater supply reliability is also hindering the growth of Europe cherry wood market. Species, such as European beech and ash, which are more abundant and faster-growing, are increasingly being stained and finished to mimic the appearance of cherry wood, capturing price-sensitive segments of the furniture and flooring markets. Simultaneously, advancements in digital printing and high-pressure laminates have enabled the production of synthetic surfaces that convincingly replicate the grain and color of cherry wood without the associated maintenance or cost. These synthetic options are particularly dominant in the mass-market housing and commercial fit-out sectors, where durability and budget constraints outweigh the desire for solid wood. The perception of cherry wood as a luxury item limits its application to niche markets, preventing broader adoption. This dual pressure from cheaper natural alternatives and sophisticated synthetics squeezes the market share of genuine cherry wood, forcing producers to constantly justify its premium pricing through superior quality and authenticity narratives.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2034 |

|

CAGR |

4.06% |

|

Segments Covered |

By Type, Application, And Region |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Baillie Lumber Co., UPM-Kymmene Corporation, Stora Enso, Binderholz GmbH, Mayr-Melnhof Holz, Pollmeier Massivholz GmbH, Rettenmeier Holding AG, Metsä Group, Södra Skogsägarna, Ilim Timber Industry |

SEGMENTAL ANALYSIS

By Type Insights

The sweet cherry tree wood segment was accounted in holding a prominent share of the Europe cherry wood market in 2025, with its status as a native European species, Prunus avium, which ensures seamless compliance with regional sustainability regulations and minimizes logistical carbon footprints. The stringent preference of European craftsmen and regulatory bodies for locally sourced timber that adheres to the EU Timber Regulation, which prohibits the placement of illegally harvested wood. The superior aesthetic and working properties of Sweet Cherry, which features a fine, straight grain and a rich color that deepens with age, making it the preferred choice for high-end joinery and restoration projects, are another factor elevating the growth of Europe cherry wood market. The wood’s moderate density allows for intricate carving and smooth finishing, qualities highly valued in the luxury furniture sectors of Italy and France.

The Brazilian cherry segment is likely to witness the fastest CAGR of 6.4% from 2026 to 2034, with the increasing demand for extremely durable hardwoods for exterior decking and high-traffic commercial flooring, where native European cherry lacks the necessary hardness and weather resistance. The first major driver is the booming outdoor living sector in Southern Europe, where homeowners seek materials that can withstand intense UV radiation and humidity without significant degradation. Brazilian Cherry boasts a Janka hardness rating of 2350, which is more than double that of Sweet Cherry, making it ideal for public spaces and luxury patios. The visual appeal of its deep reddish-brown hue, which closely mimics traditional cherry but offers greater stability and longevity, is additionally escalating the growth of the segment. The influx of FSC-certified Brazilian Cherry from managed forests in South America has alleviated regulatory barriers by allowing European importers to legally source this premium material.

By Application Insights

The furniture application segment was the largest by capturing 52.4% of the Europe cherry wood market share in 2025, owing to the enduring cultural appreciation for solid wood furniture that signifies quality, longevity, and timeless elegance across European households. The primary driver is the robust luxury home furnishings sector, where consumers are willing to pay a premium for bespoke pieces crafted from high-grade cherry wood that develops a unique patina over decades. The extensive use of cherry wood in the restoration and reproduction of antique furniture, a niche industry that thrives in countries with rich architectural histories like Italy, France, and the United Kingdom, is additionally escalating the growth of the segment. Restorers specifically require authentic cherry wood to match original components in historic estates and museums, creating a steady and inelastic demand stream. Furthermore, the versatility of cherry wood allows it to be used in various furniture styles, from traditional rustic designs to modern minimalist pieces, broadening its appeal. The material’s excellent machining properties enable manufacturers to produce complex joinery and detailed carvings that synthetic materials cannot replicate, cementing its status as the material of choice for high-value furniture production.

The flooring segment is swiftly emerging at an anticipated CAGR of 7.1% throughout the forecast period, with the rising trend of premium interior renovations and the shift toward natural, healthy living environments in residential and commercial spaces. The increasing preference for solid hardwood flooring in new luxury housing developments and high-end hotel projects, where cherry wood is selected for its warm tones and ability to enhance spatial perception. The advancement in finishing technologies has improved the durability and scratch resistance of cherry wood floors, addressing previous concerns about its suitability for high-traffic areas. Modern UV-cured lacquers and oil treatments now allow cherry flooring to withstand daily wear while maintaining its aesthetic appeal, making it a viable option for families and commercial venues. Additionally, the growing awareness of indoor air quality has led consumers to choose solid wood over synthetic carpets or laminates that may emit volatile organic compounds. This emergence of aesthetic desire, technological improvement, and health consciousness drives the segment’s exceptional growth trajectory.

REGIONAL ANALYSIS

Italy Cherry Wood Market Analysis

Italy was the top performer in the Europe cherry wood market by holding 24.4% of the share in 2025, with its world-renowned furniture manufacturing industry and deep-rooted tradition of artisanal woodworking. The nation serves as the global hub for high-end design, where cherry wood is extensively utilized in the production of bespoke kitchen cabinetry, dining suites, and luxury bedroom furniture. The “Made in Italy” brand commands a premium in international markets, necessitating the use of high-quality raw materials that meet rigorous aesthetic standards. The country’s dense network of small and medium-sized enterprises in regions like Brianza and Tuscany relies heavily on a steady supply of select-grade cherry wood to maintain their reputation for excellence. Furthermore, Italy leads in the restoration of historical interiors, where authentic cherry wood is mandatory for preserving the integrity of Renaissance and Baroque palaces. The government supports this sector through tax incentives for craftsmanship and sustainable forestry practices, ensuring a robust domestic supply chain.

Germany Cherry Wood Market Analysis

Germany’s cherry wood market was positioned second, holding 20.4% of the share in 2025, with its advanced wood processing technologies and strong commitment to sustainable forestry. The German market is characterized by a high demand for cherry wood in the production of high-quality office furniture, educational equipment, and precision musical instruments. The country’s strict adherence to PEFC and FSC certification standards ensures that nearly all cherry wood consumed is sourced from responsibly managed local forests, primarily in the Black Forest and Bavaria. The “Industry 4.0” initiative has revolutionized wood processing in Germany, enabling manufacturers to optimize yield and minimize waste when working with expensive cherry logs. Additionally, the strong domestic market for custom joinery and interior fit-outs in commercial buildings drives consistent demand. The German government’s focus on circular economy principles encourages the use of durable, long-lasting materials like cherry wood, which can be recycled or repurposed at the end of its life cycle.

France Cherry Wood Market Analysis

France’s cherry wood market growth is likely to witness a prominent growth opportunity in the coming years, with its rich architectural heritage and vibrant luxury design sector. The extensive restoration of historic chateaux, manors, and public buildings, where cherry wood is the material of choice for replicating original 18th and 19th-century joinery. In 2025, the French government allocated 400 million euros specifically for heritage conservation projects, a significant portion of which involved the procurement of authentic cherry timber for doors, paneling, and furniture, as reported by the Ministry of Culture. Beyond restoration, France is a global leader in luxury interior design, with Paris serving as a capital for haute couture home decor that frequently features solid cherry wood pieces. The country’s forestry sector, managed by the National Forest Office, ensures a steady supply of high-quality Prunus avium from mixed deciduous forests, supporting local sawmills and artisans. The French consumer’s preference for natural, eco-friendly materials aligns perfectly with the attributes of cherry wood, driving demand in the residential renovation sector. Furthermore, the presence of prestigious design schools and workshops fosters a continuous pipeline of skilled craftsmen who specialize in working with premium hardwoods.

United Kingdom Cherry Wood Market Analysis

The United Kingdom cherry wood market is expected to grow with a strong culture of bespoke joinery and the preservation of period properties. The country’s strict planning laws often require the use of authentic materials for alterations to listed buildings, creating a dedicated niche for cherry wood. Additionally, the UK has a thriving community of independent furniture makers who prioritize locally sourced timber to reduce carbon footprints and support rural economies. The Royal Institute of British Architects increasingly specifies sustainable hardwoods for high-end commercial projects, further stimulating demand.

Spain Cherry Wood Market Analysis

Spain’s cherry wood market growth is likely to grow with its growing luxury tourism infrastructure and expanding interior design sector. The use of cherry wood for high-end hotel interiors, restaurant fit-outs, and luxury residential projects in coastal regions like the Costa del Sol and the Balearic Islands. While traditionally favoring lighter woods, Spanish designers are increasingly incorporating cherry wood for its rich color contrast and durability in interior paneling and furniture. The country’s own forestry sector is improving the management of cherry tree plantations, gradually increasing the domestic supply of quality timber. Furthermore, the revival of traditional woodworking guilds in regions like Catalonia and Andalusia is fostering a renewed appreciation for solid wood craftsmanship. The export of Spanish-designed furniture featuring cherry wood to Latin American and North American markets is also gaining momentum, adding an external demand driver.

COMPETITION OVERVIEW

The competition in the Europe cherry wood market is characterized by a fragmented landscape of specialized sawmills, large forestry conglomerates, and independent traders who vie for dominance through quality differentiation and supply chain reliability. Unlike commodity timber sectors, this niche market relies heavily on the aesthetic grading of logs and the ability to provide consistent dimensions for bespoke applications, creating high barriers to entry for non-specialized players. Major competitors leverage their ownership of certified forest estates to guarantee sustainable sourcing, which is a prerequisite for supplying luxury furniture makers and heritage restoration projects. Competitive pressure drives continuous investment in precision drying technologies and optical grading systems to minimize waste and maximize the value of each scarce cherry log. Pricing strategies remain transparent yet firm due to the limited supply of mature trees, forcing companies to compete on service levels, technical expertise, and customization capabilities rather than cost alone. The threat of substitution from stained beech or synthetic alternatives requires incumbent firms to constantly emphasize the unique patina and historical authenticity of genuine cherry wood. Strategic alliances with designers and architects are common tactics to secure specifications for high-profile projects. This dynamic environment fosters a culture of craftsmanship and sustainability where reputation and trust are the primary currencies of success.

KEY MARKET PLAYERS

A few major players of the Europe cherry wood market include

- Baillie Lumber Co

- UPM-Kymmene Corporation

- Stora Enso

- Binderholz GmbH

- Mayr-Melnhof Holz

- Pollmeier Massivholz GmbH

- Rettenmeier Holding AG

- Metsä Group

- Södra Skogsägarna

- Ilim Timber Industry

Top Strategies Used by Key Market Participants

Key players in the Europe cherry wood market predominantly employ vertical integration strategies to secure direct access to high-quality forest resources and control the entire value chain from harvesting to processing. Companies frequently invest in advanced drying and grading technologies to maximize the yield and aesthetic quality of premium cherry logs, ensuring they meet the exacting standards of luxury manufacturers. Strategic partnerships with certified forest owners and cooperatives are common tactics to guarantee a stable supply of sustainably sourced timber while adhering to strict environmental regulations. Expansion into niche markets such as heritage restoration and bespoke musical instrument manufacturing allows firms to diversify revenue streams and capture higher margins. Sustainability certification under schemes like FSC and PEFC serves as a critical differentiator, enabling producers to access green public procurement contracts and appeal to eco-conscious consumers. Digitalization of supply chains improves traceability and operational efficiency, providing transparency from forest to final product. These multifaceted approaches collectively ensure long-term competitiveness and resilience in a specialized and highly regulated industry.

Leading Players in the Europe Cherry Wood Market

- Stora Enso stands as a global leader in renewable packaging and wood products with a significant footprint in the European hardwood sector. The company manages vast forest reserves and operates advanced sawmills that process high-quality cherry wood for luxury furniture and interior applications. Globally, Stora Enso contributes to sustainable construction by promoting wood as a low-carbon alternative to steel and concrete. Recent actions to strengthen its market position include the modernization of its sawmill facilities in Finland and Sweden to improve yield efficiency and grading accuracy for premium hardwoods. The corporation actively invests in digital traceability systems to ensure full supply chain transparency, meeting the rigorous demands of eco-conscious architects and designers. By integrating circular economy principles into its operations, Stora Enso enhances the value of every harvested tree. These strategic initiatives reinforce its reputation as a responsible supplier and secure its role as a key partner for high-end European woodworking industries seeking certified and sustainable cherry timber solutions.

- UPM-Kymmene operates as a pioneering force in the biofore industry, combining traditional pulp and paper expertise with innovative wood product manufacturing across Europe. The company plays a crucial role in the cherry wood market by supplying select grades of hardwood to specialized joiners and furniture makers who demand exceptional aesthetic quality. On the global stage, UPM is recognized for its commitment to carbon-neutral production and the development of new wood-based materials. Recent efforts to bolster its market presence involve expanding its network of certified forest holdings to ensure a steady supply of native cherry logs. The firm has also launched new service platforms that offer customized cutting and drying solutions tailored to the specific needs of luxury manufacturers. UPM collaborates closely with research institutions to optimize silvicultural practices for hardwood growth, ensuring long-term resource availability. These forward-thinking strategies demonstrate its dedication to sustainability and innovation, positioning UPM as a trusted partner for clients requiring reliable and environmentally responsible cherry wood supplies.

- The Schweighofer Group is a prominent European timber trader and processor known for its extensive distribution network and deep expertise in hardwood logistics. The company serves as a vital link between forest owners and high-end manufacturers, specializing in the sourcing and grading of premium cherry wood for the furniture and flooring sectors. Globally, Schweighofer influences the market by setting high standards for timber quality and sustainable trade practices. Recent actions to strengthen its position include the acquisition of strategic storage facilities in Central Europe to enhance inventory management and reduce delivery times for urgent projects. The group has also implemented advanced scanning technologies to precisely grade cherry logs, maximizing value for both suppliers and customers. These operational improvements and technological investments underscore its commitment to excellence, ensuring it remains a preferred supplier for discerning European craftsmen and industrial users seeking top-tier cherry wood.

{kind=link}