- Ongoing structural weaknesses in the timber industry and a lack of historical compounding make WOOD unattractive versus broad market benchmarks.

- Within WOOD’s holdings there is a degree of dilution of pure timber exposure, with significant allocations to packaging and materials sectors beyond forestry.

- The fund’s 0.4% expense ratio and unreliable dividend yield further diminish its appeal.

Aleksandr Potashev/iStock via Getty Images

Investment Thesis

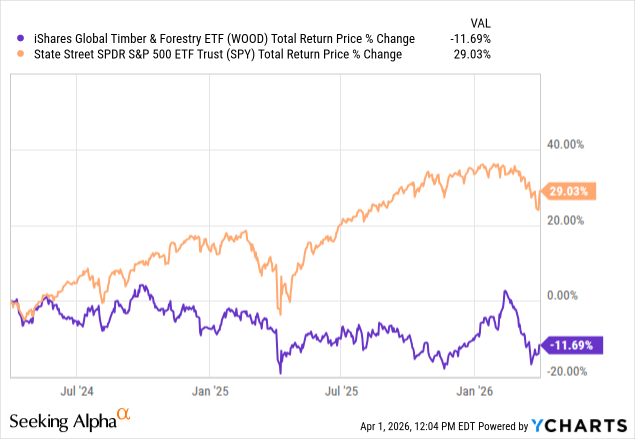

My last article on iShares Global Timber & Forestry ETF (WOOD) was published nearly two years ago, and my prediction of poor long-term performance for the fund has proven so far correct. Its 12% capital loss since my previous article compares extremely poorly with the 29% enjoyed by the broad market over the same period (as proxied by the S&P 500).

Data by YCharts

Nevertheless, I thought that, given the composition of the ETF changing significantly since my last coverage, it would be worth re-appraising the fund and looking at whether the timber sector (as proxied by WOOD) now represents an attractive value play.

Ultimately however, my up-to-date analysis concludes that ongoing structural weakness in the timber industry renders WOOD an unattractive long-term bet versus the broad market, and may actually increase portfolio risk rather than effectively offering the diversification some investors may hope it provides.

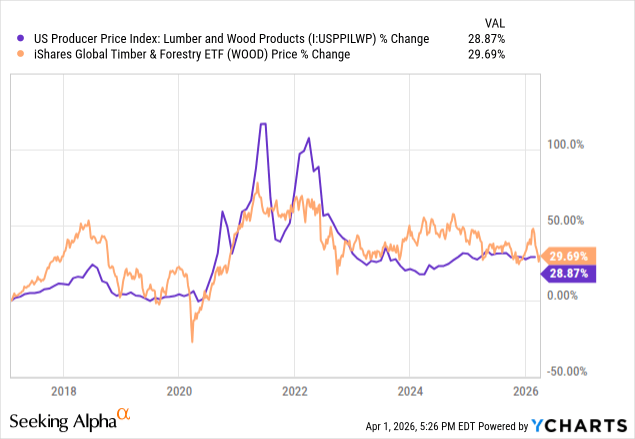

Lumber Prices

Data by YCharts

Considering that the companies owned by WOOD are mostly concerned with selling material derived from trees, it is not surprising that the ETF’s performance is linked strongly with lumber prices. As shown above, although the lines don’t overlap perfectly, the correlation is definitely strong, in the same way as the market price of gold miners or oil majors tends to align with the price of the specific commodity they are extracting and selling.

For me though, what is most striking about the graph above is that it demonstrates that over a nine-year period, in terms of capital gains,

there has been almost no difference in return between the price of the raw asset (lumber, up 29%), and the aggregate market value of the

companies producing it and turning it into products such as paper and packaging (these are up only 30%, per WOOD).

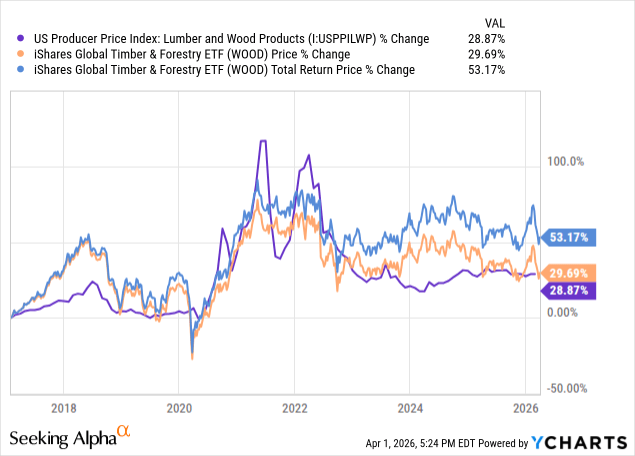

Data by YCharts

Taking into account total return (i.e. dividend reinvestment), the picture is slightly more optimistic, but it is difficult to argue that a 53% total

return from owning equities over the past nine years or so is a successful result, with the S&P offering a 234% return over the same period. What is clear is that given the commodity nature of the timber business, there is a structural issue with these firms being able to generate significant shareholder value, as illustrated by the very small long-term margin between lumber prices and timber equity prices.

Data by YCharts

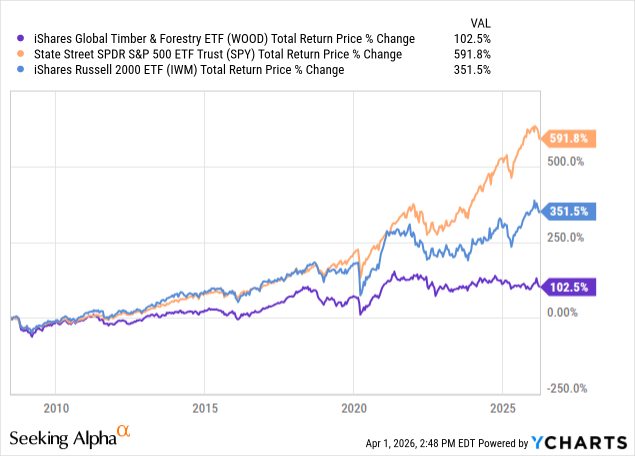

The graph since inception (24th June 2008) paints a similar picture, and underscores the reality that over the last couple of decades, there has been little evidence of WOOD’s ability to meaningfully compound capital, especially versus the tough comparison of the tech-heavy S&P 500,

but also versus small cap stocks (as proxied by the Russell 2000), and indeed by a very significant margin (with even small caps offering close

to 3.5x the return of WOOD).

Even the transport sector (as proxied by the XTN ETF), another tough industry dominated by commodity businesses, has performed better than WOOD over the years, illustrating that timber stocks definitively belong to the category of long-term capital destroyers (relatively speaking, versus other sectors).

Holdings

Clearly, it’s also important to consider the specific holdings of the fund when considering its investment merit.

Given the fund has “Timber & Forestry” in its name, one might expect it to be a pure-play timer fund, though even the sector breakdown gives

some sense of the degree to which this is not the case, with 23% of equities being classed as in the “Containers & Packaging” sector versus “Paper & Forestry Products”. This highlights that the fund owns companies at different layers within the timber value chain (some having a much greater emphasis on packaging, for example, which clearly has different economics to pure-play forestry).

WOOD Sector Exposure (Blackrock iShares)

Geographically, the fund’s largest exposure is to the United States, approaching a third of its assets. Investors should also be aware of some of the country risks associated with some of the emerging market exposures which include Brazil (at ~15%) and China (at ~6%). Taken together,

Thailand, Chile and South Africa also represent another ~7% of the fund, illustrating that the fund is absolutely a global timber play, rather than emphasizing only U.S. based firms.

WOOD Geographic Exposure (Blackrock iShares)

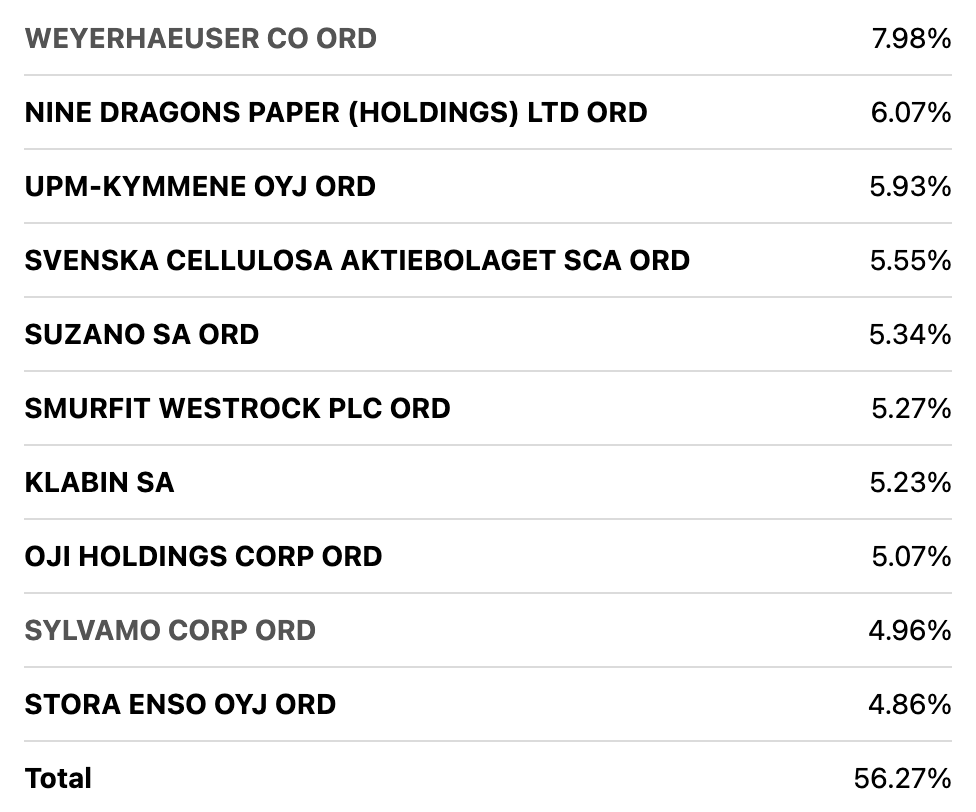

Considering some of the fund’s individual holdings is also useful for getting a sense of what prospective buyers will own.

WOOD Top 10 Holdings (Seeking Alpha)

The largest holding at ~8% of assets is Weyerhaeuser (WY), a U.S. timberland REIT with an emphasis on sustainability. Clearly, this is the sort of company one might expect to find in this sort of fund.

On the other hand, Nine Dragons Paper, at 6% of holdings, highlights the degree to which the fund is less of a pure play on timber, but rather on the wider timber value chain and associated industries (packaging). This is a firm which increasingly recovers recycled paper rather than depending purely on wood pulp.

Investor Report 2025/2026 (Nine Dragons Paper Holdings)

The fund’s third largest holding (at ~6% of assets) is UPM, another firm which is increasingly moving into materials outside of simple paper and

timber.

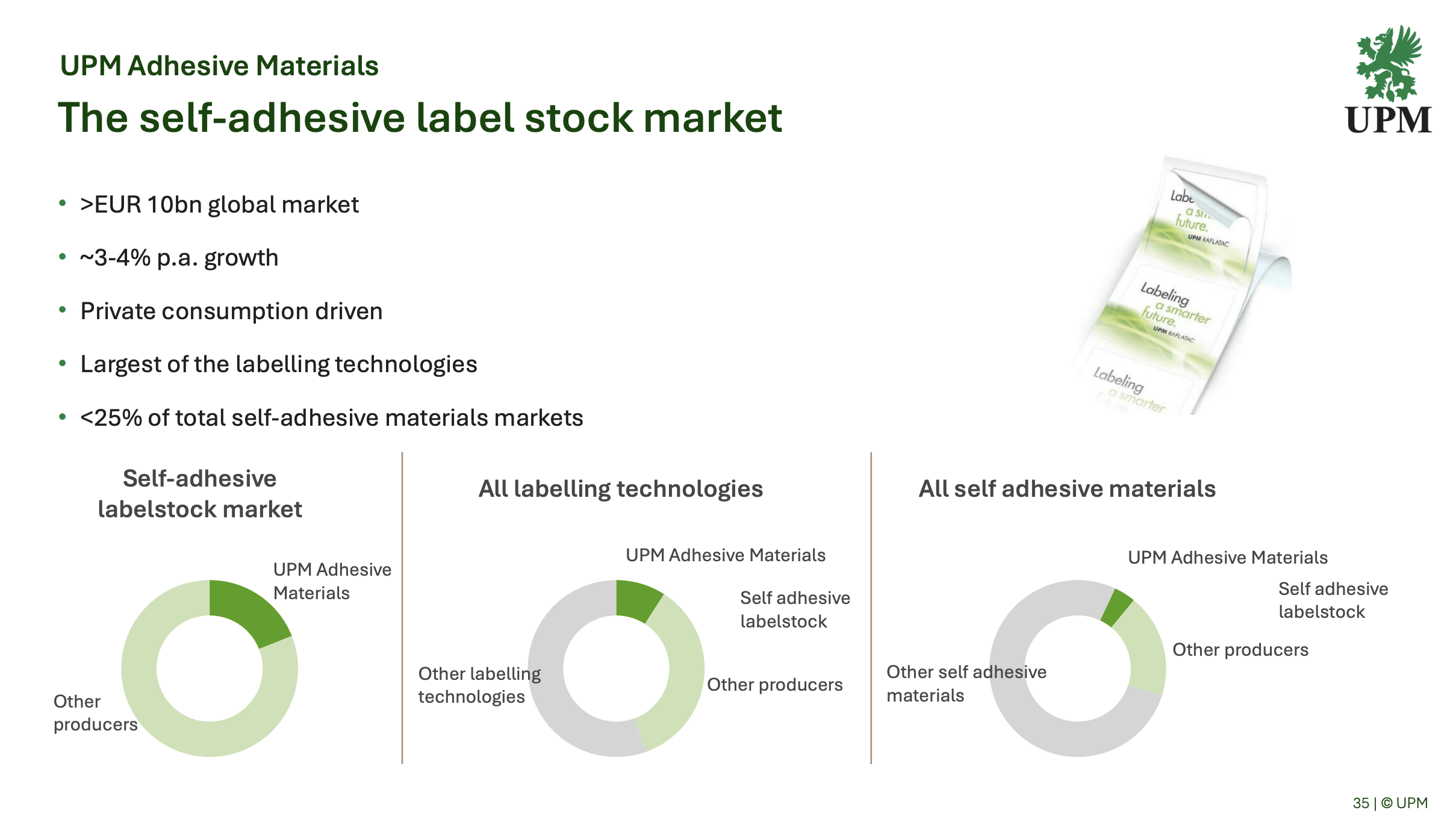

UPM Adhesive Materials (UPM Investor Presentation)

As shown above, self adhesives represent an increasing share of revenue, and while they may increase the degree to which value can be added by the firms (rather than following lumber prices), this move into the materials sector can also be seen as diluting the timber exposure offered by the fund.

Geopolitical Risk

The “elephant in the room” concerning all equity coverage at the moment is of course the Iran conflict and the potential effects of that on

different sectors.

Interestingly, the effect on WOOD is rather indirect here, and the risk is not that there is a material effect in terms of timber being transported through the Strait of Hormuz. On the other hand, there is a big potential effect in terms of the costs associated with cutting and transporting timber and lumber, where diesel, for example, is a significant input cost.

Perhaps more significantly, housebuilding is a major source of demand for wood products, and the Iran crisis has the potential to increase inflation, leading to frozen or increased interest rates (mortgage rates), which is highly negative in terms of driving the housebuilding construction which the timber industry has been holding out for over recent years.

Clearly then, prospective investors in WOOD need to pay close attention to developments around the Iran conflict and the potential inflation which may result from it, given the likely impacts on the industry.

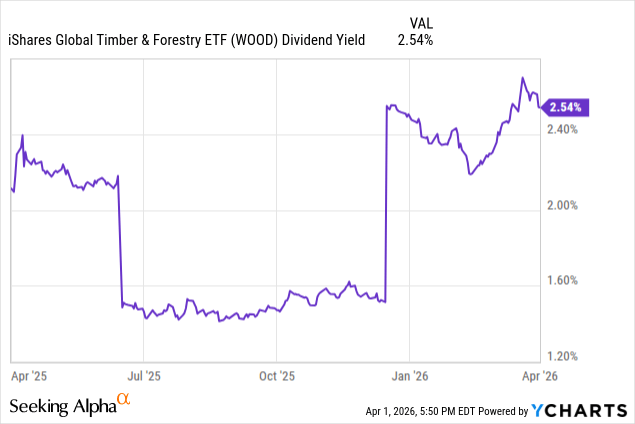

Dividends

Income investors may be drawn to WOOD on account of its 2.54% dividend yield, which is quite a bit higher than the 1.14% offered by the S&P.

Data by YCharts

On the other hand, as shown in the graph above, given that the holdings of WOOD vary over time due to rebalancing and reconstitution, this yield can’t be relied upon over the long-term. In the second half of 2025, the yield was closer to ~1.5%, which is clearly much less appealing,

relatively speaking.

I also think its important to balance the relatively higher yield offered by timber firms against the very poor capital returns I outlined earlier

in the article. With returns six times lower than the S&P 500 over less than 20 years, I think it is difficult to argue that the yield is a material consideration here.

Fees

Another aspect which investors should be aware of is the level of fees applied to the fund. While the 0.4% is slightly lower than the 0.5% average across the entire universe of ETFs, it is still at a level which materially erodes returns over time. Over a 10 year holding period, for

example, there is a ~4% loss to fees.

One could argue that for a relatively specialized, niche product with international exposure, this level of fees is not totally unresonable.

However, in the context of the 0.03% expense ratio from the S&P 500 fund from the same provider (IVV), the fees do seem a little high, especially in view of the very poor long term returns so far offered by the fund.

Upside Risk

Since I’ve presented a highly bearish view of the fund, it’s important to also be aware of the main scenario in which my thesis could be proved

wrong. Clearly, the main upside risk here would be a swift end to the conflict in Iran, which would reduce inflationary pressures and reduce

the input costs for timber businesses. A calmer geopolitical environment would also leave the path to interest rate reduction clearer, and lower

interest rates would be likely to promote the housebuilding which the timber industry relies on.

Conclusion

Overall, WOOD has provided pretty poor results over time, and I think this trend is unlikely to reverse meaningfully in the coming years, especially due to pressures on the industry on account of the current geopolitical situation. I also think the 0.4% expense ratio is not warranted and that the dividend yield should not be a material consideration for investors. Given that the fund’s holdings are diversifying into other types of materials (adhesives, for example), I also think there is an argument to be made about the purity of timber industry exposure within the fund.

{kind=link}